When applying for a personal loan, credit card, or even a mortgage in Hong Kong, you may have heard bank officers mention the term “TU.” These two letters can determine whether your loan application is approved — and more importantly, how high your interest rate will be.

In this article, we’ll break down how credit ratings (TU scores) work and share five practical strategies to improve your score, helping you save a significant amount on interest costs.

TU refers to the credit report provided by TransUnion, the main credit bureau in Hong Kong. It records your past borrowing history, repayment behaviour, and account information.

TransUnion converts your credit history into a numerical score ranging from 1,000 to 4,000, which is then classified into ten grades from A to J.

Grade A – C: Excellent credit. Banks consider you a low-risk borrower.

Grade D – F: Average credit. Loans are usually still approved, but interest rates may be slightly higher.

Grade G – J: Poor credit. Loan applications are more likely to be rejected or approved only with very high interest rates.

Many borrowers assume loan interest rates are fixed. In reality, banks use a principle known as risk-based pricing.

If your credit rating isn’t ideal, don’t worry. TU scores are dynamic, meaning they can improve over time with the right financial habits.

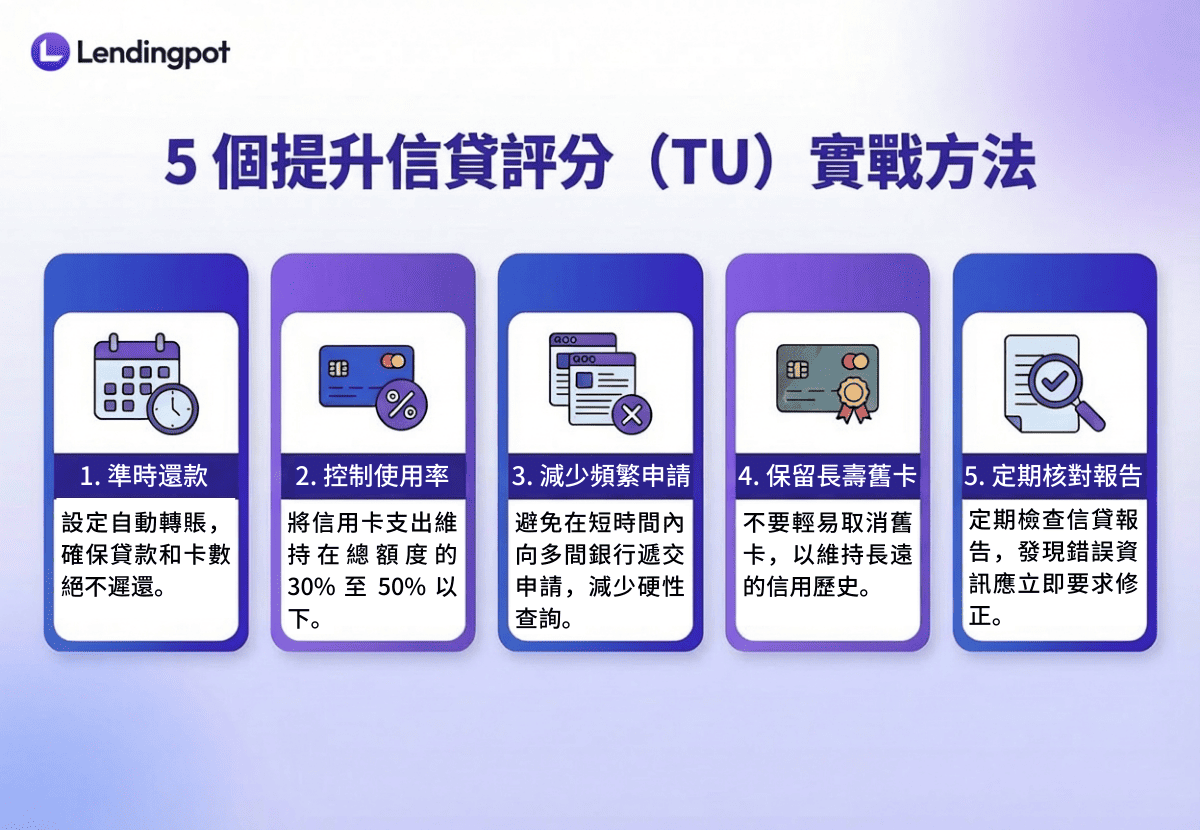

Here are five practical ways to strengthen your score:

Your repayment history carries the largest weight in your credit score.

Even being one or two days late on a credit card payment can be recorded on your credit report. Setting up automatic payments is recommended to ensure all loan and credit card payments are made on time.

Avoid maxing out your credit cards.

Ideally, keep your credit card usage between 30% and 50% of your total credit limit.

For example, if your credit limit is HK$100,000, your statement balance should preferably stay below HK$30,000.

Even if you pay on time, consistently maxing out your cards may signal financial stress and negatively affect your score.

This is a common mistake.

Each time you apply for a loan, the bank performs a “hard inquiry” on your credit report through TransUnion.

Multiple hard inquiries within a short period can significantly reduce your credit score because they may indicate that you urgently need cash.

💡 Tip: With the Lendingpot loan comparison platform, you can compare offers from 45+ licensed lenders at once. The initial matching process uses a soft inquiry, which does not affect your TU score. This helps you identify the best options before submitting a formal application.

The length of your credit history is another factor in your credit score.

If you have an older credit card that has been active for 10 years with a good repayment record, it’s usually better not to cancel it, even if you don’t use it often. A long credit history demonstrates consistent financial behaviour.

Sometimes a drop in your TU score may be caused by incorrect information — for example, if a bank fails to update your repayment record.

It’s advisable to request your credit report from TransUnion periodically and request corrections immediately if you notice any errors.

Improving your TU score doesn’t happen overnight. However, with consistent financial discipline, you could save tens of thousands of dollars in interest over time.

If you’re planning to apply for a loan but aren’t sure which bank offers the most suitable rate for your current profile, Lendingpot can help.

Our one-stop loan comparison platform allows you to quickly compare offers from major licensed lenders with transparent terms — and even enjoy up to 0.5% cashback.

Click “Apply Now” or speak with our advisory team to start your personalised loan journey today.

Lendingpot is working on making your search for financial products an easy one. Apply on our platform for personal loans, business loans and mortgage refinancing to get access to exclusive rates with our partners. On top of that, we aim to bring you insights & reviews on the latest financial products available.

.svg)